If you liked the movie “The Big Short” then you’ll want to read this. Mortgage-backed securities (MBSs) are back, and they are being bundled this time as Fix-and-Flip mortgage bonds. It’s “Wall Street’s new housing bet to boost home flippers”, says Inman’s headline on February 15, 2017.

photo by Jaap Buitendjk- (c) 2015 Paramount Pictures")

What is it? Last year Fannie Mae and Freddie Mac began to sell millions of dollars of notes (mortgages) to super-large hedge-funds. The hedge-funds keep the high performing notes, or the notes they like the best, and sell the rest to large hedge-funds, who do the same thing, and eventually these notes get down to the guy and gal in their real estate investment office, like me. Introducing myself, my name is Grace Widdicombe, real estate and note investor. I buy houses and notes on houses.

Why did Fannie and Freddie sell the notes? Because the big banks are holding way too much in loans and they need to free up their books in order to loan out more. After all, it’s in the transaction fees that the financial institutions make most of their money. That’s cash on demand, not cash down the road. So, they sell these loans at pennies on the dollar.

According to Inman’s article “Wall Street and new online lenders are bundling loans for home flippers into fix-and-flip mortgage bonds…the bonds could help accelerate a long-overdue makeover of U.S. housing stock, though not without raising eyebrows over untested financial innovations.” The article goes on to explain, “Mortgage bonds…allow large investors to buy mortgages in bulk, freeing up the balance sheets of lenders so they can fund more loans. By making it easier for fix-and-flip lenders to offload loans en mass, fix-and-flip mortgage bonds could allow lenders to make more loans at even lower rates.”

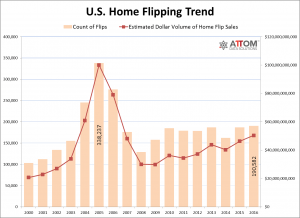

More loans could have a positive impact on neighborhoods and property values by encouraging home flippers to rehab distressed or neglected properties. The median age of U.S. homes was 37 years in 2015, according to the National Association of Homebuilders.

Christian Fuentes, co-owner of Diamond Bar, California-based brokerage Re/Max Top Producers, is quoted as saying about today’s fix-and-flip lenders; “They’re mainly looking at the actual property and the value and what you’re buying it for and your exact strategy. It’s not like a standard loan where they do a full screening on you…you can get an approval in a couple days on just the property itself.”

The Inman article notes that some observers “see a level of complexity and risk that recalls the subprime mortgage bonds of the housing boom.” Let’s keep an eye on these fix-and-flip mortgage bonds.

Read the article here: http://www.inman.com/2017/02/15/fix-flip-mortgage-bonds-wall-streets-new-housing-bet-boost-home-flippers/